Bluspring Enterprises

Why one of India's most respected investors is quietly buying a loss-making spin-off, and what he can see that the headline number hides.

Where this one started for me

Every few months a name lands on my screener that does not make sense at first glance, and Bluspring Enterprises was exactly that. A company that listed less than a year ago, that the broader market has barely noticed, sitting near its lowest price since listing, and reporting a loss. The kind of stock most people scroll straight past. What stopped me was who was buying it.

On 23 March 2026, Ashish Dhawan picked up seventeen lakh shares of this company straight from the open market and pushed his holding past six percent. For anyone who does not know the name, Dhawan co-founded ChrysCapital, one of the largest private equity firms this country has produced, and then walked away from finance to build Ashoka University. He is not a momentum trader and he is not a promoter looking to defend a price. When a man with that record buys a reported loss with his own money, and keeps adding to it quarter after quarter, the correct response is not to dismiss the stock. It is to ask what he can see that the rest of us are missing.

This report is my attempt to answer that question honestly, running the business through my usual eight stages, and to decide whether I would put my own capital next to his. I will tell you up front that the answer is yes, but with conditions, and the conditions matter more than the verdict.

Stage 1 | Understanding the business

Bluspring was carved out of Quess Corp through a composite scheme that took effect on 31 March 2025, and the stock began trading on its own on 11 June 2025 at around 89 rupees. Strip away the new name and what you are looking at is the integrated services arm of Quess, now standing on its own feet. It is a people business at its core, employing more than 93,000 workers across 28 states, and it sells the unglamorous but essential work that keeps offices, factories, airports and food courts running.

The company operates through six brands, and it helps to know what they actually do rather than treat them as a logo wall. Avon handles facility management, the cleaning, upkeep and engineering of buildings. Indya runs food services and institutional catering. Terrier provides manned and technology-led security. Hofincons does industrial maintenance for plants and heavy assets. Vedang services the telecom tower and network side. And then there is Foundit, the old Monster jobs portal for India and Asia, which is the odd one out and the single most important thing to understand about this company.

How the money comes in

Most of the revenue is contractual and recurring, which is exactly the quality I look for. A factory does not stop needing housekeeping next quarter, and an airport does not switch its security vendor on a whim. The largest engine is Facility and Food Services, which brought in 2,031 crore in FY26 and grew twelve percent, adding eighty new contracts worth 313 crore of annual value. Telecom and Industrial Services contributed 615 crore and is moving toward outcome-based contracts where Bluspring is paid for uptime rather than headcount, which is a healthier model. Security Services grew a steady eight percent. Foundit, the job platform, did just 78 crore.

Stage 2 | Industry and macro backdrop

The tailwind here is genuine and it is structural, not a story. India is in the middle of a long, slow formalisation of its services economy. Companies that once hired cleaners, guards and canteen staff informally are outsourcing these functions to organised players, partly for efficiency and increasingly because of compliance. The new labour codes, GST and tighter audit norms all push work toward the few firms that can handle payroll, statutory dues and documentation at scale. The integrated facility management and business services market in India is estimated at around 1.7 lakh crore and growing at roughly thirteen percent a year.

That is the good news. The honest part is that this is a low-margin, fiercely competitive arena. Bluspring sits alongside SIS, Updater Services and its own former parent Quess. Customers have real bargaining power, contracts can be re-bid, and a meaningful share of the cost base is simply wages passed through. Nobody in this industry earns software margins. The winners are decided by scale, by the ability to cross-sell five services into one client, and by the discipline to keep collections tight. Growth is available to everyone. Profitable growth is not.

Stage 3 | The moat, such as it is

I want to be careful here because it is easy to talk a thin moat into a wide one. Bluspring does have advantages, but they are of the modest, accumulating kind rather than the fortress kind. The first is switching cost. Once a client hands over its entire facility, food, security and maintenance stack to one vendor, ripping that out is painful and risky, so contracts tend to renew. The second is the compliance barrier. Running 93,000 people across 28 states with clean statutory records is genuinely hard, and it quietly disqualifies the small local operators that compete on price alone. The third is the cross-sell, where one relationship becomes four service lines.

What the business does not have is pricing power. It cannot raise rates at will, and a determined competitor can undercut on any single service line. So I score the moat as narrow but real. It is the kind of edge that protects existing revenue and helps win the next contract, not the kind that lets you expand margins simply because you are dominant. For a company like this, the moat is a reason the revenue is sticky, not a reason the stock will compound on its own.

Stage 4 | Management and the smart money

The promoter is Ajit Isaac, the man who built Quess Corp into one of India’s largest staffing and services groups. That lineage matters. Bluspring is not a first-time promoter learning the business on listed-company money. It is a seasoned operator who has already built and scaled exactly this kind of platform once before, now doing it again with a cleaner slate. The promoter group holds close to 58 percent, so management’s interests are firmly tied to the share price. Day to day, the company is run by Kamal Pal Hoda as Executive Director and CEO.

Why I keep coming back to Dhawan

This is where the report really lives. Dhawan’s buying is not a one-off. He moved from roughly four percent, to five percent, to 6.10 percent across successive quarters, and the March purchase of seventeen lakh shares was a clean open market transaction disclosed under the takeover regulations, not a demerger allocation that fell into his lap. He was buying while the stock sat near its lowest level since listing, around 51 rupees. A foreign fund, Ellipsis Partners, was nudging its stake up alongside him, and Tata Mutual Fund had been accumulating earlier. This is patient institutional money building a position into weakness, which is the opposite of what a crowd does.

I do not buy a stock because a famous investor owns it. That is how retail money gets trapped. But when a disciplined value buyer accumulates steadily into a falling price, it is a strong signal to do the work and find out why, because he has usually found something the screen does not show. In this case he has.

Stage 5 | The financials, and the loss that isn’t

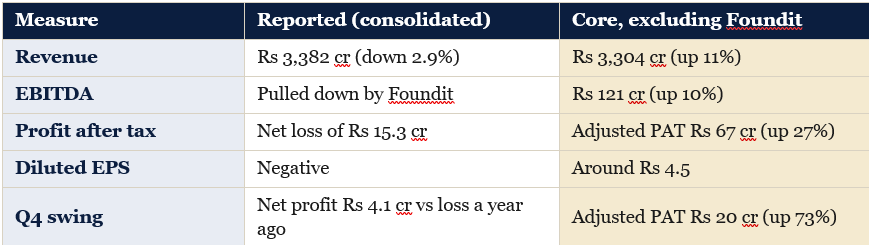

Here is the headline that scares people away. For the full year FY26, Bluspring reported a consolidated net loss of about 15 crore on revenue of 3,382 crore. On the surface, a loss-making company with flat revenue. Most investors stop reading there. That is the mistake, and I think it is precisely the mistake Dhawan is being paid to exploit.

Dig one layer down and the picture inverts. The entire loss is coming from one segment, Foundit, the old jobs portal. In FY26 Foundit did 78 crore of revenue against an EBITDA loss of around 43 crore. It is a digital turnaround project sitting inside a services company, and it is bleeding. Now strip Foundit out and look at the core business that actually employs the 93,000 people and signs the contracts.

The two faces of FY26

So the real operating business earned 67 crore last year, up 27 percent, and it is the consolidated number that is in the red only because Foundit’s losses sit on top of it. That single distinction is the whole investment case.

The trajectory underneath is also turning. Quarterly EBITDA margin moved from 3.5 percent in the second quarter to 4.2 percent in the fourth, and the March quarter for the consolidated entity actually swung to a small net profit of 4.1 crore, against a loss in the same quarter a year earlier. Even Foundit showed its first green shoots, with fourth-quarter billings of 26 crore, about half again above its prior run rate, after a product revamp. The full-year loss collapsing from 172 crore in FY25 to just 15 crore in FY26 tells the same story from the top down.

The blemish I will not paper over is cash and capital efficiency. This is a working-capital-heavy business, debtor days spiked after the demerger as contracts were novated to the new entity, and return on equity over the last three years is barely above zero. Debtor days have since improved from around 83 to 59, which is encouraging, but the quality of earnings here is low, and I treat the reported numbers, not the adjusted ones, as the conservative anchor.

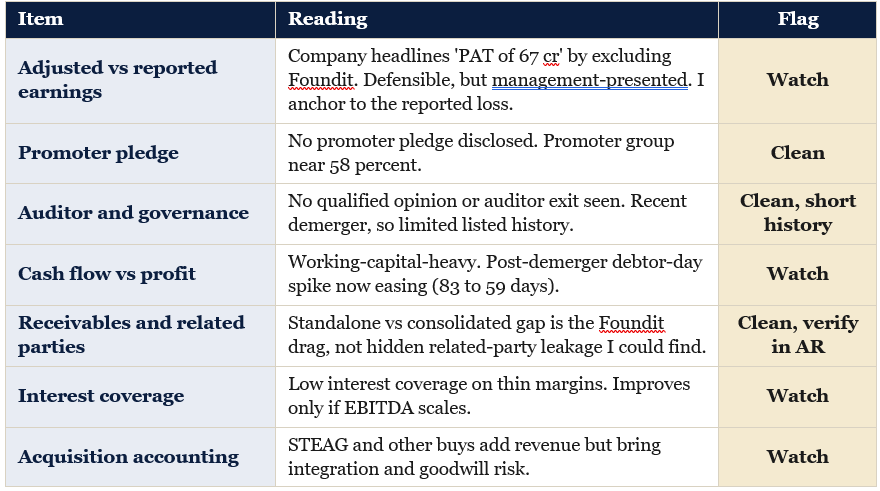

Stage 6 | Forensic checklist

This is the stage where I try to talk myself out of the idea. With a loss-making, recently demerged company that leans on an adjusted profit figure, scepticism is not optional. Here is the checklist, run honestly.

Nothing here is a thesis-breaker, which is more than I can say for some of the names that get pushed as smart-money plays. The honest verdict on the forensic stage is that the risks are about quality and execution, not about integrity. The one discipline I would impose on myself is to read the full FY26 annual report for the exact net debt, the operating cash flow figure, and any related-party receivables before sizing the position up, since I worked off the results filing and summary financials for those.

Data gaps I am flagging openly: precise net debt, full-year operating cash flow, and the segment split of the order pipeline. Verify these in the annual report before acting.

Stage 7 | Valuation

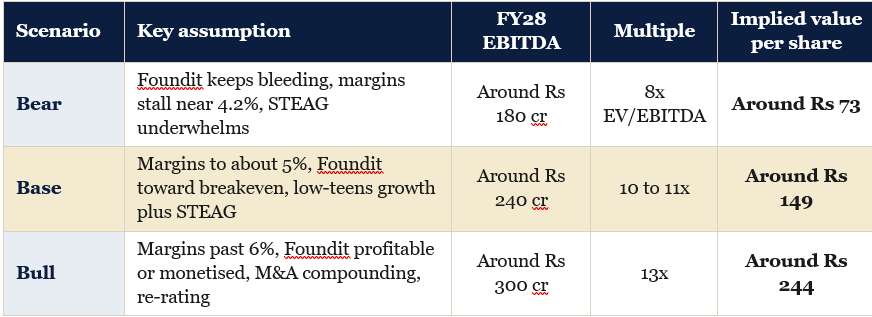

A discounted cash flow on a company that barely breaks even on a reported basis would be false precision, so I am not going to pretend otherwise. The cleaner way to value a thin-margin services roll-up is on what the business can earn once the Foundit drag fades and margins inflect, and then to sanity-check that against what comparable services firms fetch on enterprise value to EBITDA. I have run three scenarios out to FY28 and shown my assumptions, because you should be able to argue with them.

Weighting these at thirty percent bear, fifty percent base and twenty percent bull gives me a probability-weighted fair value of about 145 rupees per share, against a current price near 73. That is roughly a fifty percent discount to fair value, which is the margin of safety my framework demands before I will act.

Two honest caveats on this number. First, the entire base and bull case rests on margin expansion and on Foundit stopping the bleed, neither of which is proven yet, so this is an earnings-recovery valuation, not a steady-compounder valuation. Second, the easy money has already been made. The stock has run from a low near 44 to about 73 since the demerger washout, so the violent mispricing Dhawan stepped into is partly closed. What is left is a still-attractive, but no longer screaming, discount.

The risks I am underwriting

— Foundit may never turn. If the jobs portal keeps losing 40 crore or more a year, the adjusted profit story stays adjusted forever and the consolidated entity stays loss-making.

— Margins are structurally thin. Facility management is a four percent business on a good day. The base case needs five percent or more, and that is not guaranteed in a price-competitive market.

— Reported revenue actually fell in FY26. The growth lives in the core, but the headline can stay uninspiring and keep sentiment weak.

— Acquisition risk. STEAG and the other deals add scale but bring integration, goodwill and execution risk, and acquisitions are where services roll-ups most often stumble.

— Working capital and cash. Until I see clean operating cash flow in the annual report, I treat the cash conversion as unproven.

— Smart money is not a guarantee. Dhawan can be early, or wrong, and an investor with no lock-in can exit without warning. His position validates the work, it does not remove the risk.

What I am watching each quarter

Three numbers will tell me whether this thesis is working. First, the Foundit EBITDA loss, which needs to shrink toward zero rather than widen. Second, the consolidated EBITDA margin, which needs to hold above four percent and ideally climb past five. Third, operating cash flow against reported profit, which needs to show the business converting its earnings into actual cash. If those three move the right way over the next two to three quarters, the verdict strengthens and the position can grow. If Foundit’s losses widen or margins slip back, I will step aside without ceremony, because at that point it is just a low-margin services company on a turnaround that did not turn.

Disclaimer

I am not a SEBI registered investment adviser or research analyst, and nothing in this document is investment advice, a recommendation, or an offer to buy or sell any security. This is my personal, educational research, written to share how I think about a business. I hold the NISM Series XV Research Analyst certification, but that does not make this advice. The figures here are drawn from public sources including company filings, the FY26 results, exchange disclosures and Screener, and while I have tried to be accurate, figures can carry errors or change after publication, and several items remain to be confirmed against the full annual report. Markets carry risk and you can lose money. I may hold or transact in the securities discussed. Please do your own research and consult a registered adviser before making any investment decision.